The Greenhouse Gas Protocol is considering one of the most significant changes to corporate climate accounting in years: moving from a single greenhouse gas inventory toward a multi-statement reporting framework through its proposed Actions & Market Instruments (AMI) standard.

At Beyond, we strongly support this direction.

For years, companies have been forced to fit an increasingly complex set of climate actions into a reporting architecture that was never designed for today’s reality. Businesses are investing not only in reducing their own operational emissions, but also in supplier decarbonization, clean energy procurement, methane abatement, carbon removals, environmental attribute certificates, and broader climate finance mechanisms that extend beyond their direct value chains.

A single inventory cannot adequately capture all of those activities — nor can it communicate them clearly to investors, regulators, customers, or civil society.

The move toward multiple climate statements is therefore an important and necessary evolution. It creates the opportunity for companies to report climate action more transparently, more credibly, and in ways that better reflect how decarbonization actually happens in the real world.

But the success of this framework will depend heavily on how those statements are designed.

The Core Problem: Organizing Around Accounting Methods Instead of Real-World Meaning

While we strongly support the GHG Protocol’s direction of travel, we believe the proposed structure in the recently released White Paper needs to be rethought.

One of our biggest concerns is that it organizes disclosures primarily around accounting methodologies — particularly the distinction between “attributional” and “consequential” accounting.

While those concepts are familiar to technical experts, they are not how most users interpret climate disclosures.

Investors do not ask whether an intervention is attributional or consequential. Regulators do not think in those terms. And companies do not make strategic decisions based on accounting categories alone.

Instead, stakeholders want to understand a few much more intuitive questions:

- What are a company’s actual emissions?

- What actions is the company taking to reduce them?

- Are those actions occurring inside the company’s value chain?

- Are they associated with suppliers, sectors or products?

- Or are they broader climate finance efforts occurring beyond the value chain?

Those distinctions matter because they reveal very different things about risk, operational exposure, transition strategy, cost, and long-term decarbonization pathways.

Yet under the current proposed structure from GHG Protocol, fundamentally different interventions would end up grouped together on the same statement simply because they rely on similar accounting approaches.

This creates unnecessary confusion, and we have already seen even sophisticated actors misinterpret the purpose and intent of the different statements.

Instead, the structure should be designed around clarity and real-world meaning, not accounting taxonomy, so that fundamentally different types of action are not obscured by technical classification.

Why Value Chain Relevance Matters

Not all climate action is the same. There is a major difference between:

- a company helping decarbonize its own supply chain,

- a company investing in value-chain associated mitigation,

- investing in interventions associated with its sector,

- purchasing external carbon credits,

- or financing mitigation completely outside its value chain.

All of these actions can play important roles in global climate mitigation. Beyond strongly supports the continued use of carbon credits and recognizes their importance in mobilizing finance and accelerating emissions reductions globally.

But they should not all be treated as interchangeable.

Value-chain interventions are often harder. They can require supplier engagement, operational changes, infrastructure investment, long contracting timelines, and significantly higher costs. In many sectors, they represent the difficult work of driving system transformation.

If those interventions are aggregated together with lower-cost external mitigation options under a single consequential “impact” statement, companies may face growing pressure to prioritize whichever activities produce the cheapest reportable outcomes, rather than those that transform the systems their value-chains are dependent on.

That would create the wrong incentives. The world needs both:

- ambitious investment inside value chains, and

- robust financing for mitigation beyond value chains.

A reporting framework should preserve incentives for each, and not unintentionally encourage substitution away from more transformational value-chain action.

For that reason, we believe climate disclosures should be structured around value chain relevance and functional purpose, not simply accounting method.

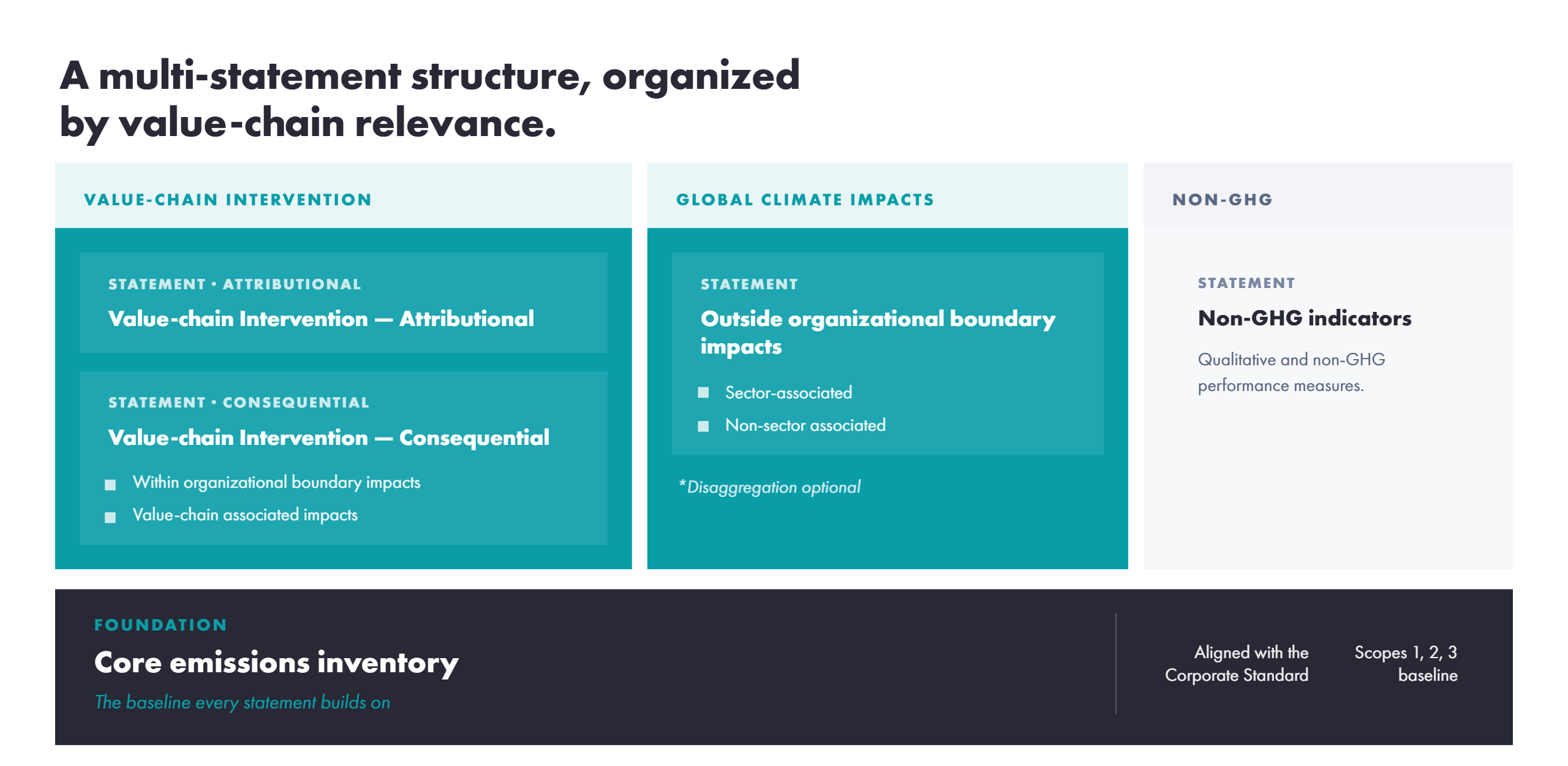

A Better Structure for Multi-Statement Reporting

Many Beyond members believe the AMI framework would become far more intuitive and decision-useful if it were organized around a simpler logic:

- A Core Emissions Inventory

The foundational inventory aligned with the existing Corporate Standard.

- Value Chain Intervention Statements

Two separate statements under a single ‘Value-chain Associated’ category that includes attributional and consequentially accounted-interventions. We strongly support the AIM Platform Standard and Guidance for determining value-chain association.

- Global Climate Impact Statements

Separate reporting for broader climate mitigation actions occurring beyond the value chain, including qualified carbon credits and an optional disaggregation for interventions that are sector-associated.

This approach would be easier for companies to implement, easier for regulators and investors to interpret, and more aligned with how climate strategies are actually designed and evaluated.

Most importantly, it would avoid conflating fundamentally different categories of climate action.

The Importance of Regulatory Relevance

Another critical issue is whether AMI becomes embedded in the mainstream reporting architecture — or remains a niche voluntary framework.

Today, most climate disclosure regulations specifically reference the GHG Protocol Corporate Standard, and only the Corporate Standard. If AMI sits outside that system, adoption is likely to remain fragmented and inconsistent across regulatory regimes.

That is why we believe the GHG Protocol should explicitly position AMI for regulatory use from the outset—either by integrating it into the Corporate Standard itself, or by creating clear, authoritative cross-references so that AMI-aligned statements can be directly recognized within regulatory disclosure requirements that reference the Corporate Standard. The framework should not be limited to informing voluntary reporting or target-setting; it should be designed to be readily usable by regulators as part of an optional but compliance-grade disclosure.

Building on Existing Work Instead of Starting Over

The good news is that GHG Protocol does not need to build this entirely from scratch. Significant work has already been done by initiatives like the AIM Platform and TCAT, which have spent years testing multi-statement approaches through company pilots and multistakeholder engagement.

Those efforts have already explored:

- eligibility criteria,

- safeguards,

- traceability requirements,

- implementation practicality,

- and methodological design choices.

Phase 2 of AMI should build directly on those learnings rather than duplicate them. Doing so would accelerate progress while grounding the framework in practical, real-world experience.

A Critical Opportunity

The transition to multi-statement climate reporting is one of the most important opportunities in corporate climate accounting in over a decade. Done well, it could significantly improve transparency, better reflect real climate action, and unlock stronger incentives for near-term decarbonization. But to succeed, the framework must remain intuitive and decision-useful. It must help users understand what companies are actually doing — not simply how accountants or ivory tower academics categorize the math.

The future of climate reporting should make corporate climate action easier to understand, not harder. And with a few changes, we think the AMI proposal is well-positioned to achieve that.